A certificate of Capital Importation (CCI) is a document issued by the Central Bank of Nigeria (CBN) to foreign investors in Nigeria as proof of their capital investment in the country. The CCI serves as a key tool for foreign investors to access various benefits and incentives the Nigerian government provides to encourage foreign direct investment (FDI) in the country. In September 2017, the CBN introduced the electronic CCI (e-CCI) which replaced the paper CCI. In this article, we will discuss the relevance of the CCI to foreign investors in Nigeria.

The CCI serves as proof of investment for foreign investors, providing them with a legal document that confirms their Investment in Nigeria. This can be used as evidence of investment for various purposes, such as opening a bank account, obtaining a loan, or applying for a Nigerian visa. Additionally, the CCI is a requirement for foreign investors to access various incentives and benefits provided by the Nigerian government, such as tax holidays and duty waivers.

One of the main benefits of the CCI is that it enables foreign investors to access the Nigerian foreign exchange market. The CCI is required to open and operate a foreign currency account in Nigeria, which allows foreign investors to transact in foreign currency without restrictions. This is particularly important for foreign investors who need to make payments or receive income in foreign currency.

The CCI also enables foreign investors to repatriate their capital and profits out of Nigeria. The Nigerian government has put in place strict regulations to ensure that capital is not moved out of the country illegally. The CCI serves as proof of legal capital importation and is required to process the remittance of capital and profits out of Nigeria.

Another relevance of the CCI is that it helps track Nigeria’s foreign investment. The CBN issued the CCI and kept it in the bank’s records, providing a clear picture of the amount of foreign investment in the country. This helps the Nigerian government to monitor and track the inflow of foreign investment and make necessary adjustments to attract more foreign investment.

In conclusion, the CCI is a vital document for foreign investors in Nigeria as it enables them to access various benefits and incentives provided by the Nigerian government and enables them to transact in foreign currency without restrictions, repatriate their capital and profits, and track the inflow of foreign investment in the country. Obtaining a CCI is a key step for foreign investors looking to invest in Nigeria and should be done as soon as possible after the investment is made.

For assistance in processing the Certificate of Capital Importation. Feel free to contact us

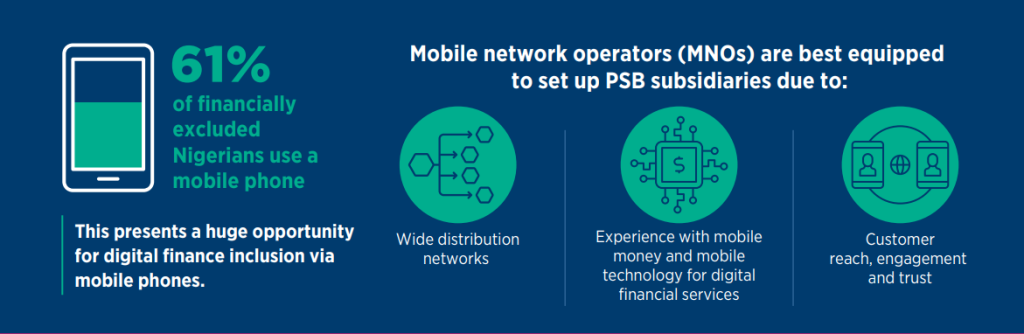

36% of Nigerian adults are unbanked. CBN aims for 95% financial inclusion by 2024. 92% of the nation’s adult male population have mobile phones while 88% of the adult female population have mobile phones.

RATIONALE

CBN aims “To enhance financial inclusion in rural areas by increasing access to deposit products and payment/remittance services to small businesses, low-income households and other entities through high-volume low-value transactions in a secured technology-driven environment.”

PSBs IN NIGERIA

As at the time of writing this article, there are five (5) PSBs in Nigeria namely 9 PSB (a subsidiary of 9Mobile), Hope PSB (A Subsidiary of Unified Payments) , Money Master PSB (A Subsidiary of Globacom), Momo PSB (A Subsidiary of MTN Nigeria), SmartCash PSB (A subsidiary of Airtel Nigeria).

REGULATORS OF PSB

The Central Bank of Nigeria is the main regulator of PSBs in Nigeria, Deposits are also Nigeria Deposit Insurance Corporation (NDIC) insured.

SERVICES PSBs CAN CARRY OUT

Accept deposits from customers and small businesses

Hold funds in an electronic wallet

Invest in an interest-bearing FBN and CBN securities and offer saving products

Provide POS and ATM Services

Build a network of physical banking agents for deposits, payments and withdrawals

Issue prepaid and debit cards

Provide inbound remittance services

Engage in different forms of local payments including merchant payments, bill payments ad person-to-person transfers.

SERVICES PSBs CAN NOT CARRY OUT

They are not to issue loans, advances and guarantees.

They are also not allowed to trade in foreign exchanges except for remittances

They are also not allowed to issue insurance products.

REGISTRATION REQUIREMENTS FOR PSBs

Steps to obtain a PSB license from CBN

Obtain the Grant of Approval-in-Principle (AIP)

Obtain the Grant for a Final Banking License

REQUIREMENTS FOR THE GRANT OF APPROVAL IN PRINCIPLE (AIP)

Formal application for the grant of a Payment Service Bank license addressed to the Governor of the CBN attached with a proposal to be submitted to the Director, Financial Policy and Regulation Department (FPRD), CBN. The proposal shall contain the business case, vision and strategy, corporate governance arrangements, risk management, compliance; and financial viability.

A non-refundable application fee of N500,000 (five hundred thousand Naira only) in bank draft, payable to the Central Bank of Nigeria or such other amount as the CBN may specify from time to time

Evidence of capital contribution made by each shareholder

Evidence of name reservation with the Corporate Affairs Commission (CAC)

Detailed business plan or feasibility report

The draft copy of the company’s Memorandum and Articles of Association (MEMART)

A written and duly executed undertaking by the promoters that the bank will be adequately capitalized for the volume and character of its business at all times, and that the CBN shall have powers to supervise and regulate its operations

Shareholders’ agreement providing for disposal/transfer of shares as well as authorization, amendments, waivers, reimbursement of expenses

Statement of intent to invest in the bank by each investor

Technical Services Agreement

Detailed Manuals and Policies, particularly

For corporate investors as the promoters shall forward the following additional documents:

Certificate of Incorporation and certified true copies of other incorporation documents

Board resolution supporting the company’s decision to invest in the equity shares of the proposed bank

Names and addresses (business and residential) of owners, directors, and their related companies, if any; and

Audited financial statements & reports of the company and Tax Clearance Certificate for the immediate past 3 years.

Where all the above requirements have been met, the CBN shall notify the applicant of its decision within 90 days. When the CBN is pleased with the application, it will grant the applicant an Approval-in-Principle (AIP).

Afterwards, the Applicant shall register the PSB with the Corporate Affairs Commission with a 5 Billion minimum share capital.

REQUIREMENTS FOR THE GRANT FOR A FINAL BANKING LICENSE

The applicants of a planned PSB must apply to the CBN for the grant of a final license not later than six (6) months after receiving the A.I.P. The application shall be accompanied by the following:

A non-refundable licensing fee of N2,000,000.00 (Two Million Naira Only) in bank draft payable to the Central Bank of Nigeria

Certified True Copy (CTC) of Certificate of Incorporation of the bank

CTC of MEMART

CTC of Form CAC 1.1

Evidence of the location of the Head Office (rented or owned) for the take-off of the business

Schedule of changes, if any, in the Board and Shareholding after the grant of AIP;

Evidence of ability to meet technical requirements and modern infrastructural facilities such as office equipment, computers, and telecommunications, to perform the bank’s operations and meet CBN and other regulatory requirements;

Copies of letters of offer and acceptance of employment in respect of the management team;

Detailed resumes of top management staff;

Completed Fitness and Propriety Questionnaire; and sworn declaration of net worth executed by top management staff;

Bank Verification Number (BVN) and Tax Clearance Certificate of each top management staff;

Comprehensive plan on the commencement of the bank’s operations with milestones and timelines for the roll-out of crucial payment channels; and

Board and staff training program.

Following that the above requirements have been met, the central bank of Nigeria shall conduct other inspection, which includes: checking the physical structure of the building, verifying the capital contributions of the promoters, meeting with the Board and Management team whose resumes had earlier been submitted to the CBN, check the original copy submitted in support of the license.

For bespoke consultation on setting up a Payment Service Bank in Nigeria